On a recent cloudy Saturday afternoon, CSI Prop hosted yet another exciting and fun Investor Club event, honouring the King of Fruits and the pride of all Malaysians: a Durian Party in recognition of the favourite season of the year!

The party, held at DurianBB Park KL, was a smashing success. The place was packed with investors and their family members who arrived in excited anticipation of the durian spread. As the theme suggests, this day was all about indulging in durian and its greatness.

On the menu were sweet, pulpy, mouth-watering varieties of durians and delicacies made out of durian such as pies and tarts. Other tropical fruits like mangosteens, nangka and rambutans were also served alongside multi-flavoured ice-creams and fresh coconut juice.

Different types of durian served for the investors and their families

The party kick started with a free flow of durian to every table where investors, alongside their family and friends, relished in the variety of durians, ranging from the mildest-tasting to the rich and creamy Musang King.

Ever the affable host, CSI Prop Director, Virata Thaivasigamony fleeted from table to table to greet and chat with guests. He then gave his welcome speech, where he shared about his own investment journey and some informative insights on the UK property and investment market.

Bonding through durian party

Sam Lee of Capricorn Financial Consultancy and our guest speaker from the UK, spoke about the current state of the mortgage market, the various financing terms available and the lending criteria for property investment in the UK.

Sam Lee during his sharing

Switching gears, we had a short and sweet session on how to pick and sample durians according to its intensity of taste, courtesy of DurianBB Park’s Stella Heong. For example, did you know that the Musang King is the strongest-tasting durian and should be eaten last? Neither did we. Stella also shared that durian and mangosteen, being the ‘fruit couple’, should always be eaten together so that the heat from the durian can be neutralized by the juicy mangosteen.

What’s a party without games? Investors were invited to participate in a durian-tasting game and stand a chance to bring home a free durian. Our investor, Mr Alex Goh, was the winner, guessing correctly in just a matter of minutes!

Are they able to guess the durian?

The durian party was clearly a hit, judging by how quickly more than 200kg of durian were consumed (on top of other fruits and pastries!) and the gleeful smiles on the faces of our guests. The evening closed with our guests receiving a goodie bag of durian snacks.

Missed out on the last Investor Club event? Stay tuned for our next one in Q4 and wait for your invitation via email!

The CSI Prop Investor Club is open to all clients of CSI Prop. It is a platform for knowledge, fun and networking and is a realisation of our core values of Knowledge, Service and Having Fun.

By Lydia Devadas Michael

Additions and edits by Vivienne Pal

UK rents are expected to increase by 15% over the next 5 years, according to research by the Royal Institution of Chartered Surveyors (RICS).

The survey observed that smaller landlords were quitting the buy-to-let sector, affecting supply. “A reduced pipeline of supply will gradually feed through to higher rents,” RICS Chief Economist Simon Rubinsohn said.

Meanwhile, the supply of rental property in the UK continues to fall. In 2017, buy-to-let properties were sold at a rate of only 3,800 a month, leading to the first drop in the number of homes available to rent in 18 years, according to the latest report from the Ministry of Housing.

In total, the number of privately rented homes in England fell by 46,000 last year — the largest reduction since 1988.

Buy-to-let properties decreased drastically last year. Source: Thisismoney.co.uk, Ministry of Housing, Communities and Local Government

The drop is attributed to the UK Government’s recent tax measures which, among others, increased stamp duty and reduced landlord relief claims against mortgage interest. The stamp duty changes have made it more expensive to purchase a buy-to-let property, and tax relief is set to drop further yearly until the 2020-21 tax year.

These changes have made it less profitable for UK landlords, especially those on a mortgage, to rent out their properties. House prices have also grown faster than rents, prompting many landlords to exit the sector. Trade association UK Finance highlighted a 19% fall in new mortgages approved for buy-to-let homes in the UK.

Demand continues to rise, and rents are expected to spiral over the next few years. This points the way towards the purpose-built rental sector as a replacement for the traditional buy-to-let properties, which are often older houses on the outskirts of city centres, geared toward owner-occupiers.

Still, rental properties located in prime city centre locations remain attractive to young working professionals who are unable to purchase their own homes. These rental properties are set to rise in the face of dwindling buy-to-lets.

Developing cities in the UK regions like Manchester, Birmingham and Liverpool are growing quickly, and properties in the city centre offer access to business opportunities, employment, and entertainment demanded by a modern working lifestyle.

While interest rates remain low, investors looking towards the UK can thus take advantage of the shortage in supply for rental properties, investing in prime locations in developing cities where the demand is the highest.

Manchester, Liverpool and Birmingham are the best places to invest in the UK. Click on the hyperlinks embedded into the cities if you want to learn more. If you are interested to explore investing in regional UK property for high returns, don’t hesitate to give us a call at +65 3163 8343 (Singapore), +603 2162 2260 (Malaysia), or email us at info@csiprop.com!

Manchester has chalked up yet another feather in its cap. The northern city now ranks among the world’s top 10 most popular cities for global investment, according to IBM’s latest Annual Report on Global Location Trends.

The report, IBM’s eleventh, tracked the movement of investment flows and its impact on economic growth around the world. This latest accolade adds credence to Manchester’s track record as one of the fastest-growing cities in the UK.

Along with Liverpool, Manchester attracted 68 foreign direct investment (FDI) projects in 2017, beating other global cities like Toronto and Barcelona. Specialisms in cyber security, FinTech and advanced materials helped the city bring the largest number of investments into the UK, second to London.

The report echoes the EY Attractiveness Survey UK 2017/18 which ranked Manchester as the most successful city to attract FDI outside London. Manchester also retained its place as the UK’s Most Liveable City in the Economist Intelligence Unit’s 2018 Global Liveability Ranking.

Manchester is the fastest-growing city for house prices in the UK, followed by Liverpool. Source: Hometrack, June 2018

The UK is currently placed fifth in the list of the worlds’ most influential FDI destinations. Britain was also ranked fifth for FDI job creation, with 51,500 new jobs born out of these global investments. Manchester and Liverpool jointly created 7,000 jobs last year.

Tim Newns, Chief Executive of MIDAS, Manchester’s inward investment agency, said: “This report once again confirms Manchester as a globally significant business destination and, together with Liverpool, illustrates the potential of the Northern Powerhouse.

“Greater Manchester is ambitious, visionary and passionate about the future. Billions of pounds are being invested to create inspiring, connected business environments that support innovation and reflect future needs, and ensure that the region continues to be a draw for the world’s most innovative companies and biggest brands.

“Talent is one of the key attractors for global businesses and with student retention figures at an all-time high in Manchester, it is creating an even more compelling case for investment.”

In August, Booking.com, the world’s third largest e-commerce company announced a £100 million investment into a new global HQ in Manchester, with online health and beauty retailer The Hut Group (THG) also announcing plans to move into MediaCityUK.

This weekend, find out more about this amazing project in Manchester and how you can profit from it.

This weekend, learn how you can invest £75K & GET BACK £190K in 5 YEARS with the POWER OF LEVERAGE! Come for the EXCLUSIVE WORLD LAUNCH of an iconic new residential development in the Manchester city centre – THE CROWN On Manchester’s Skyline. Call +60162288691 to book your seats now!

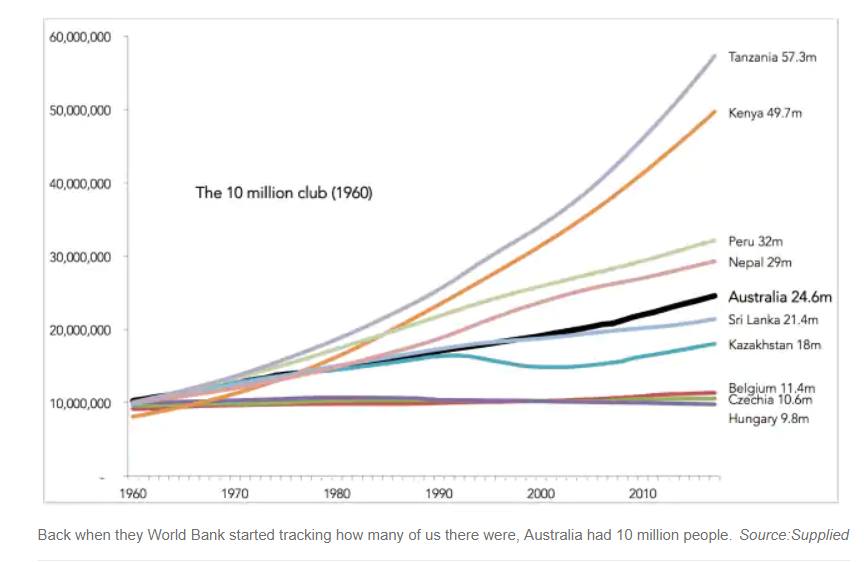

Compared to developing nations with far stronger population growth rates, Australia is expanding pretty quickly for a developed country.

Last month, Australia’s population officially ticked past the 25 million mark, according to the latest data by the Australian Bureau of Statistics (ABS) – 33 years earlier than projected!

Over the last three years, the nation’s population grew by around 400,000 people per year. If this trend continues, the number might reach 26 million in the next two to four years. This is no mean feat considering that the population Down Under was only at the 10 million mark back in 1960.

Back in 1960, the Australian population totalled only 10m. Today, the population number has ticked over the 25 million mark. For a developed nation, Australia’s population growth rate is quite incredible! Source: Supplied & News.com.au

Nett migration has continued to outpace births, with the highest migrant numbers coming from China and India.

Newly elected Minister for Cities, Urban Infrastructure and Population, Alan Tudge, in outlining plans for the country’s immigration policy, is not in favour of reducing skilled migrant numbers.

“My view has always been that Australia can be a bigger country. But, ideally, you have a broader distribution rather than very rapid growth in some areas,”he said.

Melbourne and Sydney are expected to grow to the size of New York city by 2050 as migration numbers continue to grow.

To date, Melbourne has the fastest-growing population rate in the country. Naturally, this has something to do with Melbourne’s ranking as the World’s Most Liveable City for seven consecutive years, receiving a perfect score from The Economist for healthcare, education and infrastructure.

“There’s a buzz about the city that keeps bringing the world’s best to enjoy Melbourne,” said the Australian government in a statement.

Victoria has an estimated population of 5.71 million, ranking second in the country with a population density of 25 people per sq km. The state accounts for 25% of the entire Australian population.

And, for the first time ever, Victoria finally overtook New South Wales as Australia’s strongest economy in CommSec’s latest State of the States report.

Victoria’s high population growth has also supported house prices and rental values in Australia, and is a reason why the Melbourne market has remained strong.

In quarterly data by JLL Australia, apartment price growth for Greater Melbourne (for both new and existing stock) increased 6.6% y-o-y to 1Q2018, which is above the five-year annual average rate of 4.5%. Rental vacancy remains tight in the city.

The recent 2018 Global Real Estate Transparency Index by JLL ranks Australia’s property market as the most transparent in the Asia-Pacific region. This, and the all the things that make Australia such an attraction — good governance, strong healthcare and education systems, etc — are a great draw for property investors and millionaires.

What do you think of Australia’s population growth for the Australian economy and property market as a whole? Leave your comments in the box below! For more details on investing in Australian property, call us at 65-3163 8343 (Singapore), 03-2162 2260 (Malaysia), or email us at info@csiprop.com!

By Noorasikin Ali

Additions & Edits by Vivienne Pal

One of the latest movies to hit the cinema, Crazy Rich Asians, features the members of the wealthy Young family, who are termed “not just rich, but crazy-rich”. As the story goes, the family made their fortune through investing in property.

Yes, property is tangible and finite – there’s only so much of it on this planet, so it will always be in demand. But some places are better than others. As any seasoned property investor will tell you, location is perhaps the most important thing to consider for the best returns.

In Singapore, house prices as a whole have dropped 5% since 2011. Some areas have been hit more heavily than others. One of the worst hit was Sentosa Cove, where average prices were down by almost 30% from their 2011 highs.

Residential property on the island city remains highly regulated, and a string of cooling measures by the Government this February put a halt on the short run of growth since last year. In Q3 2018 prices went up by 0.5%, compared to the 3.4% rise in Q2.

Other than the slowdown in growth, an additional hit on property investment in Singapore is that local and foreign buyers now have to pay an extra 5% in stamp duty, further reducing returns.

Right now local property investment appears to be giving less-than-stellar returns. So, if not in Singapore, where then can Singaporeans looking to be crazy-rich put their money?

Currently the exchange rate for the pound sterling is at S$1.81 to £1 (15 Oct). Prior to the 2007 Financial Crisis, the exchange rate hovered at around S$3 to £1.

GBP to SGD over last 20 years (Exchange Conversions)

This means that essentially, the UK is on sale for Singaporeans — at a 40% discount — compared to a decade ago!

The UK is also facing its biggest ever housing shortfall — in England alone, there is a total backlog of almost 4 million homes.

Research by Heriot-Watt University shows England must build 340,000 homes per year until 2031 to meet demand — a figure significantly higher than the government’s estimates.

This shortfall in housing is not new, and multiple failures of the UK Government to spur the house-building industry have caused prices to soar. House prices in the UK grew 32.28% over the past 5 years, and a whopping 323.58% over the past 25 years!

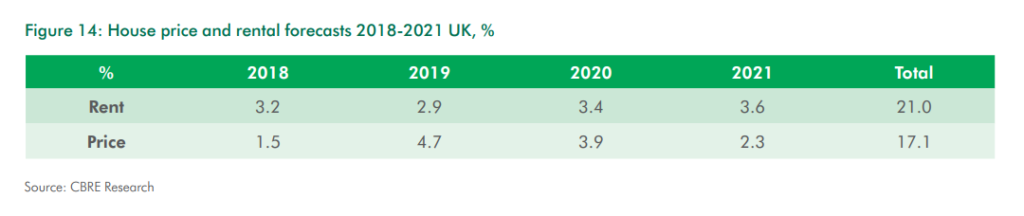

CBRE Research predicts house prices to continue to rise. For the next 3 years, house price growth is estimated to increase by 17.1%, while rental is expected to grow by 21%.

UK house price and rental forecast 2018-2021 (CBRE)

Regional cities in the UK are great places to invest in real estate, as their frenzied pace of development continues, compared to the over-saturated market of London.

These British regional cities have shown the most promising growth: over the past 12 months since June, Manchester clinched top spot at 7.4%, followed by Liverpool at 7.2%, and Birmingham at 6.8%. Compared to these, the capital only managed a dismal 0.7%.

Price growth of UK cities in last 12 months (Hometrack)

As long as supply is unable to keep up with demand, prices will continue to rise. For the foreseeable future, England’s shortfall in housing is not going to be solved soon, and Singaporeans can take advantage of the currency rate and purchase UK real estate —at adiscount!

Are you looking to invest in UK real estate? Don’t hesitate to give us a call at 65-3163 8343 (Singapore), 03-2162 2260 (Malaysia), or email us at info@csiprop.com!

Few can truly grasp the magnitude of that sum of money. But we could try and give you a rough idea in property terms!

With $1 billion, you can get 4585 homes in Manchester at a cost of £166,000* per home. With a rental yield of 5.90% p.a.** and annual capital growth of 7.4% p.a.*, that $1 billion can get you total returns of £2 billion*** in 7.5 years!

*Hometrack, June 2018

**Private Finance

***Total value of asset + 7.4% capital growth + 5.90% annual rental yields over 7.5 years.

Now that’s a whale of an investment! Why just blow it all away when you can put it into a growth asset and double your investment!

Got $1 billion to spare and fancy blowing it on some property? Give us a shout! Or let us know in the comment box below what you would spend your money on!

You’ve thought long and hard, and have decided to invest in UK property. What happens next? This article will guide you through the different stages of the UK property investment process.

It starts with choosing a property that fits your budget and investment goals and appointing an agency that can take you through the purchase process. Unless you don’t mind the hassle of traveling to and from the UK to deal directly with the developer/seller, a good agency will help you select developers carefully, i.e those with a good track record of completing projects on time.

It is important that your agent works closely with the developers, facilitating communication from the developer to you, and vice versa.

1: Property Reservation

Documents and payments to reserve a UK property with CSI Prop

We recommend investments based on your goals and budget, and once you have decided on the property for investment, you will need to sign Reservation Forms and a Solicitors Appointment Letter.

Several payments are required at this stage:

Reservation Deposit*: approx £5,000 (forms part of the purchase price, non-refundable)

Administration Fees: £800

Legal Fees*: Between £700 to £2000

*Payment can vary depending on project/developer/solicitor

CSI Prop works closely with a panel of recognised solicitors in the UK. We’re happy to recommend our panel, but you may use solicitors of your own choosing.

Before proceeding with the contracts to purchase your property, your solicitor will activate the Anti-Money-Laundering process.

2: Anti-Money-Laundering Checks

Anti-Money-Laundering documents that will need to be submitted

The Anti-Money-Laundering process is a very important part of buying UK property, and is done by your solicitor on behalf of the UK Government to ensure that your purchase funds are not related to suspected money-laundering and terrorism links. Your solicitor will ask for proof of your identity, residential address, availability of funds and its sources.

3: Exchange of Contracts & 1st Payment

Once you have completed the Anti-Money-Laundering process, you will need to sign the Sale and Purchase Agreement. This is normally done within 28 days of your solicitors receiving the contract from the seller’s solicitors. Together with this Agreement, you will make your first payment to the developer via your solicitors. This amount varies from one developer to another.

Progress payments apply for some projects, e.g. UK commercial student property, and the timelines for these payments will be stipulated in the Agreement.

4: Financing

You may apply for financing while purchasing UK residential property with a value in excess of £100,000. Application for financing can be done 3 to 6 months before settlement, and the banks will assess your financing position and eligibility. Documents which are typically required by the bank include:

3 to 6 months salary slips

3 to 6 months bank statements

Income Tax Return Form

There are typically no application and processing fees to finance your property. However, the legal fees can incur up to 1.5% of the value of your property. There are several banks in Malaysia and internationally that offer financing. Please get in touch with us to find out more.

5: Final Settlement & Stamp Duties

When your property is nearing completion, the developer will send a Completion Notice to your solicitors. You will need to make full payment for the property at this stage, which is also known as the final settlement, and pay any applicable stamp duties to HM Revenue & Customs (HMRC).

Stamp duty is a percentage of the property price, which varies based on the value of the property, and whether it is categorized as residential or commercial (e.g. UK commercial student property or care homes).

CSI Prop can recommend a tax agency to assist with filing and paying the tax on your behalf. Otherwise, you can file the return and pay the taxes yourself.

Stamp Duty for UK Residential Property

You will be entitled to stamp duty rebates if this is your first or only residential property purchase globally. Most investors already own a house, hence the following stamp duty rates will apply:

Stamp Duty for Individuals Owning Multiple Houses

Stamp Duty for UK Commercial Property

For commercial property, you don’t pay any stamp duty up to £150,000. You pay stamp duty of 2% for the next £100,000 (the portion from £150,001 to £250,000). Any portion above £250,000 is charged at 5%.

Buying Commercial Property as an Individual

6: Property Management

When you exchanged contracts with the developer, you may have signed an agreement to hire a letting agent. You may also have chosen to manage the property yourself.

The letting agent will ensure your property is well-maintained, taking care of all expenses involved, and collecting the rental on your behalf.

Note that a condition applies when buying UK property with a rental assurance (such as UK commercial student property). Buyers will have to use the letting agent prescribed by the developer for the whole duration of the assurance period to qualify for the rental assurance.

7: Rental Income

You will need to pay income tax to the UK Government once your property starts generating rental income.

We can recommend a qualified professional in the UK to manage your taxes. You may also file your rental income taxes to HMRC through self-assessment (using form NRL1).

You may be eligible for the standard personal allowance if it is included in the double-taxation agreement between the UK and the country you live in. This is the amount of income you don’t have to pay tax on every year. For example, Malaysians qualify for this allowance but Singaporeans do not.

You get a standard personal allowance of £12,500 (as per 2019/20), unless your income is £100,000 or above. The allowance decreases incrementally (see table below) if your income is above £100,000.

Your personal allowance can vary if you apply for Marriage Allowance or Blind Person’s Allowance.

Personal Allowance in the UK

You pay 20% tax on the first £50,000 of your income, after deducting any personal allowance.

For example, if you have the standard personal allowance of £12,500, you pay 20% tax on the next £37,500 of your income. If you do not have any personal allowance, you are taxed at 20% on the first £50,000 of your income.

For the the portion from £50,001 to £150,000, you pay 40%, and for the portion above £150,000, you pay 45%.

UK Tax Bands

8: Property Resale/Exit

Should you choose to sell off your property, we can recommend a property agent and solicitor to assist you.

The agent’s commission rates, your advertising budget, and exclusivity will be decided by you and the agent. The agent will provide an appraisal of the property indicating how much they expect to sell the property for, and tell you how they plan to market your property. Agents normally charge between 2% and 3% of the sale price of residential property, whilst the resale of commercial student property can cost up to 5% of the sale price due to the smaller price quantum of the property. This rate can be negotiated.

The solicitor’s fees will start from approximately £2,000, depending on the value of your property.

Take note that, unlike stocks, property is not a liquid asset, and you should always expect that it will take some time for the property to be sold.

The sale of UK property is subject to Capital Gains Tax (CGT).

Capital Gains Tax (CGT)

Capital Gains Tax (CGT) is paid on any gains you make when you dispose of your property.

Your taxable gain is the difference in price between the purchase and sale of your house, after taking away any allowable expenses and your personal allowance (if selling as an individual).

All non-UK residents get an annual personal allowance of £12,000 for CGT (as per 2019/20).

Allowable expenses include the stamp duty paid upon the purchase of the property, agent fees and legal fees incurred during the purchase or sale, and payments for valuations made on the property.

For residential property, CGT is taxed at 18% on your gain if your total taxable income is £50,000 and below, or 28% if more:

Example:

Jason sells his apartment for £275,000. He had previously bought it for £200,000, giving him a total cash gain of £75,000.

Jason must report the sale to HMRC, complete a full CGT computation and pay any CGT within 30 days of transfer.

Jason’s expenses come up to £30,400, and after deducting his personal allowance, has a total taxable gain of £32,600.

Since his total taxable income is less than £50,000, he will be taxed on his gain at the CGT rate of 18%. This will come up to a tax of £5,868, or 2.13% of the apartment’s sale price.

Example of Capital Gains Tax calculation

Click here for more guides on property investment, and please subscribe to our website notifications to get the latest updates! Leave us a comment below if you have any thoughts or questions on our article.

If you are interested to explore investing in UK property for high returns, or if you need us to refer you to a good tax firm in the UK, don’t hesitate to give us a call at (65) 3163 8343 (Singapore), 03-2162 2260 (Malaysia), or email us at info@csiprop.com!

Disclaimer: This guide is an outline of CSI Prop’s purchase process, which may differ from other consultancies. CSI Prop does not provide tax & legal advice and accepts no liability. Readers are encouraged to consult a qualified tax or legal advisor for a thorough review. You should also seek advice based on your particular circumstances from independent advisors and planners.

Exactly one week ago, Malcolm Turnbull saw his three-year reign at the helm replaced by former treasurer Scott Morrison, following much political chaos within the ruling Liberal party. Australians and foreign investors alike will be keeping an eye on what happens to the economy and housing market. Here’s a snapshot of the new Australian PM.

Former treasurer, Scott Morrison is Australia’s new Prime Minister, replacing Malcolm Turnbull who stepped down after three years following a bitter tussle in the Liberal Party leadership.

Scott Morrison, or ScoMo, is also Australia’s 30th Prime Minister — the sixth, in fact, in the last 11 years alone. In a closed-door meeting of Liberal lawmakers last week, Morrison won 45 votes to 40 over right-wing populist Peter Dutton. Morrison was known as the most conservative members of the Liberal’s moderate wing.

ScoMo the Regular Joe

The Prime Minister is an observant pentecostal Christian who grew up in a Christian home, in the beachside suburb of Sydney. Married with 2 daughters (after a long 18-year wait and 10 attempts at in vitro fertilisation), Morrison had a brief career as a child actor, appearing in several TV commercials. He achieved some notoriety as managing director of Tourism Australia when he approved an $180m international advertising campaign that was subsequently banned in Britain for crass language.

ScoMo on Politics & Immigration

Morrison’s exposure to politics began at a young age. At 9, he handed out “how to vote” pamphlets on behalf of his father, a former policeman and local councillor who served as mayor for a spell. He was elected member of parliament in 2007, holding several positions in government, including minister of Social Services, minister of Immigration & Border Protection and, up until last week, Treasurer.

ScoMo was (in)famously an ardent supporter and enforcer of a contentious policy which turned away immigrants who tried to enter Australia illegally by boat. These asylum seekers were detained in offshore camps.

Conversely, when it comes to skilled migrants, Morrison is clearly a supporter and was known to rebutt former Prime Minister Tony Abbott’s proposal to cut migration rates.

According to Abbott, the current intake of permanent migrants had affected house prices and wage growth in Australia. He suggested that immigration numbers to be cut by 80,000 a year.

The suggestion did not sit well with ScoMo who felt that Australia had benefitted tremendously from skilled migrants.

“If you cut the level of permanent immigration by 80,000 it would cost the budget, it would hit the bottom line — the deficit — by $4 billion to $5 billion over the next four years,” Morrison quickly countered.

“Basically the economy (would not be) growing at the same level and people who come as skilled migrants pay taxes, make a net contribution to the economy.

“Currently two-thirds of permanent migrants have skills needed by the economy. A cut in overall numbers would reduce the skilled total and emphasise family migration which ultimately gets more dependent on welfare,” he added.

Australia’s foreign migrant inflow continues to drive the growth of the housing market.

ScoMo & the Housing Market

Morrison is a supporter of APRA’s regulatory controls, believing that it would help in rebalancing the market. This, according to an analysis in the Australian Financial Review, is part of what makes him a “property person’s prime minister”. He is no stranger to real estate, having worked as national policy and research manager for the Property Council of Australia for 6 years and, according to industry captains, has “shown a deft touch in managing fears around the overheated investment market”.

Morrison is well aware of the conditions of the housing market in Australia but holds a firm belief that the country is not headed towards a housing market crash, citing APRA’s regulatory controls to credit access will help create a smooth landing.

To date, Australia holds the record for not going through a recession for 26 years. During ScoMo’s watch as Treasurer, Australia’s economy grew 1% in 1Q2018 and 3.1% annually, placing Australia on top of advanced economies in terms of economic growth.

Looking Ahead

Up until now, not a single Australian Prime Minister has completed a full term. The frequent upheavals have left foreign allies uncertain, according to experts.

In his speech, the newly minted prime minister said, “We will provide the stability, the unity, the direction, and the purpose that the Australian people expect from us.”

What happens from here is anyone’s guess. There are supporters and naysayers on both sides of the political divide, but ScoMo has, at the very least, until May 2019 when the country goes to the polls, to prove himself and the Liberal Party worthy.

How do you think Scott Morrison will fare as the new Prime Minister of Australia? Share your thoughts with us in the comment box below. If you’re keen to learn more about investing in Australian property, call us at 016-228 8691/ 9150 (MY) or (65) 3163 8343.

By Noorasikin Ali

Additions & Edits by Vivienne Pal

Today marks Pakatan Harapan’s 100th day in power since the political earthquake that shook Malaysia — the 14th General Election.

The pressing question is whether the nascent government has delivered on its word and lived up to the expectations of Malaysian voters thus far.

The last three months for Pakatan has been like a walk on the proverbial tightrope, with the coalition struggling to deal with the threat of bailing investors and a sovereign downgrade, and a national fiscal debt that has turned out to be more critical than expected.

A survey carried out by the Merdeka Centre earlier this month (August 2018), found that Malaysian citizens were largely satisfied with Pakatan Harapan ministers, but with some concerns about the economy, and racial and religious rights.

As part of its election manifesto, the government had pledged to deliver 10 promises in 100 days, but not all of these promises have been fulfilled.

Tun Dr Mahathir Mohamad, the Prime Minister, said that the reason behind the government’s inability to fulfil the 10 promises was because they had to prioritise other important matters.

“The government’s focus is not only on the 10 promises in 100 days, the government has a lot of work to do and this includes ‘cleaning up’ the government which was tainted with corrupt practices and abuse of power during the past administration,” he said.

Harapan Tracker, a website which monitors the government’s performance, gave Pakatan a score of 45%, a cumulative average from its two scores of “the letter of the promise” (30%) and “the spirit of the promise” (60%).

Housing Not Part of 100-day Pledge

The housing sector, in particular, was not included in Pakatan’s list of 100-day promises.

Many Malaysians are concerned about housing, and rightly so. There has been a glut of high-end residential property and a scarcity of affordable housing in the country — an imbalance that has caused many Malaysians, especially those from the bottom 40% of income earners (B40), to be unable to afford their own homes.

Pakatan’s 10 pledges to be achieved in 100 days

Dr Carmelo Ferlito, an economist with the Institute for Democracy and Economic Affairs (Ideas) said the spectacular growth of the high-end property segment was ignited by rising profit expectations, growing demand and easy credit conditions.

“The mix of elements generated a bubble which reached its peak between 2012 and 2013.”

Zuraida Kamaruddin, the new Housing Minister, has embarked on a consolidation of all affordable housing projects under the Ministry in an effort to streamline the building of affordable homes. Certain projects like the 1Malaysia Housing Programme (PR1MA) were previously placed under the Prime Minister’s Department.

The new National Affordable Housing Council is expected to begin its work this month (August 2018) once papers regarding its set-up are finalised by the Cabinet. The council will monitor the construction of affordable housing, coordinate databases and implement a self-renting scheme for the B40 and M40 (middle 40% of income earners) groups nationwide.

Ms Zuraida also plans to set up a one-stop online platform for affordable housing that would enable buyers to submit an application online, and find out their approval status within days.

In an effort to further bring down the price of housing in Malaysia, Finance Minister Lim Guan Eng announced that building materials and construction services will be exempted from the upcoming Sales and Service Tax (SST). The SST is set to kick in on Sept 1.

Under the previous Goods and Services Tax (GST) regime, building materials and construction services were subjected to a 6% tax. However, players in the construction industry are not optimistic that the tax exemption will impact house prices significantly.

Datuk Steve Chong, chairman of the Real Estate and Housing Developers’ Association (Rehda) in Johor, thinks that the exemption is insufficient to bring down the prices of homes.

“We believe that the savings is too small to be passed on to homebuyers which will not in any way translate to a significantly lower price for homes in future,” he said.

Malaysian Institute of Architects (PAM) president Ezumi Ismail added that raw materials only accounted for less than a third of the total development cost, and other factors contributed to high housing prices.

“The rest … would consist of the cost to purchase the land and other compliance charges that come with the building the houses or units. SST may reduce the house prices but it may not be much.

“Some projects require the developers to construct basic infrastructure and facilities that are supposed to be built by utility companies. The added cost would then be (pushed) back (to) the consumers. It would be better if the authorities come up with a building master plan that could address these issues,” he added.

A new National Housing Policy is expected to be announced in September with a considerable number of changes, one of which includes the rental-tenancy market.

The rising supply of residential properties, particularly condominium and apartment units, has caused rentals to continue to drop in Kuala Lumpur.

Previndran Singhe, CEO of Zerin Properties said, “It is a tenant market right now as they have plenty of choices. There have been drops in rental in KL, generally around 10%.”

“Some owners have to reduce their rents because their units are already old and they will not be able to compete (with newer properties) if they don’t upgrade their homes.”

Silver Lining

There isa silver lining in sight. Yet, it may be a long while before housing issues are fully addressed in the country. Until then, what stands to remain is the loftiness of house prices in prime areas like the Klang Valley and Penang — and to a certain extent, Johor Bahru — which will impact not just first home buyers, but also local property investors.

With economists slashing economic growth forecasts due to weak economic data (ahead of Bank Negara Malaysia’s release of GDP 2Q2018 figures), and potentially more fiscal tremors ahead, a single 5-year term may not be enough for the government to make the changes it wants to.

Investors should continue to maintain a wait-and-see stance before embarking on investment-related decisions in the local property market or, alternatively, look beyond Malaysian shores. Virata T of CSI Prop says that investors can still get good returns on properties in countries abroad.

“With rental yields dropping locally, investors wanting to invest in property could look overseas to get better returns on investments. There is a rising interest among Malaysian investors for this type of investment,” he said.

“Up-and-coming cities in countries with a stable economy like the UK and Australia, are particularly attractive as they provide good returns while reducing investors’ exposure to economic risk.”

What do you think of Pakatan’s performance so far? Leave us a comment below!

If you are curious about investing overseas and the returns you can obtain thanks to low vacancy rates, call (+65) 3163 8343 (Singapore), 016-228 8691/ 9150 (Malaysia), or email us at info@csiprop.com!

The Bank of England raised interest rates for the second time in under a year. What does this signal and how will it affect the UK housing market?

The Bank of England (BOE) has raised interest rates to 0.75%.

The hike was the second since the 2008 financial crisis. Last November it rose to 0.5% from 0.25%, the first time in almost a decade.

The BOE Monetary Policy Committee, which decides interest rates, voted unanimously for an increase in rates following positive economic growth and an encouraging labour market.

BOE Governor Mark Carney told reporters that economic growth rebounded in the second quarter, after a slight slowdown at the start of the year.

The bank’s forecasts show that consumer price rises could reach 2.2% in 2019 and 2.1% in 2020.

The BOE is likely to increase rates further if its forecasts prove right. Any future rise in rates, however, is likely to be at a gradual pace and to a limited extent.

This points to continued stability in the real estate market.

Andrew Burrell, JLL EMEA Head of Forecasting, says: “The (rate) rise has been largely priced in and is not expected to have major impact on real estate markets.” He observes that there will be more pressure on yields from market rates eventually.

Despite the rate hike, returns from real estate continue to remain attractive when compared to other asset classes.

Working in favour of the UK real estate market is the employment rate and stable consumer confidence, as well as the OECD predictions of global GDP growth at 3.8% for this year.

Sterling set to rise?

The falling pound dropped to its lowest level against the euro in nearly a year last week on 9 Aug, but edged higher against the Euro to 1.12 this week (as of 16 Aug).

Sterling’s fall against the Euro and the Dollar (Source: BBC)

Stabilization of the pound could be due to the rate hike, which usually pushes up its value, and news reports detailing the potential for a concession being put on the table by the EU in the ongoing round of Brexit negotiations.

Some member states are reportedly ready to allow Britain to remain in the single market for goods while opting out of the free movement of persons. The trade-off is that the UK replicates all new EU environmental, social and customs rules in addition to those set out in Theresa May’s Chequers proposal.

This marks the first major divergence between the European Council, which is made up of leaders from member states — and the European Commission. The concessions will be discussed at a meeting of leaders from both sides in Salzburg this September.

The currently weak pound provides foreign investors with a window of opportunity to buy into UK property and obtain good returns.

Jeremy Stretch, head of FX strategy at Canadian Imperial Bank of Commerce said the pound typically underperformed during the August holiday period. CIBC had tracked the pound’s performance on a monthly basis over the last 15 years.

Following this trend, foreign investors who are interested in UK property may want to consider entering the market now before the pound starts to rise again.